A short while back, I explained how, in our fervor to rapidly expand charter schooling and decrease the role of large urban school districts in serving their resident school-aged populations, we’ve created some particularly ludicrous scenarios whereby, for example – charter school operators use public tax dollars to buy land and facilities that were originally purchased with other public dollars… and at the end of it all, the assets are in private hands! Even more ludicrous is that the second purchase incurred numerous fees and administrative expenses, and the debt associated with that second purchase likely came with a relatively high interest rate because – well – revenue bonds paid for by charter school lease payments are risky. Or so the rating agencies say.

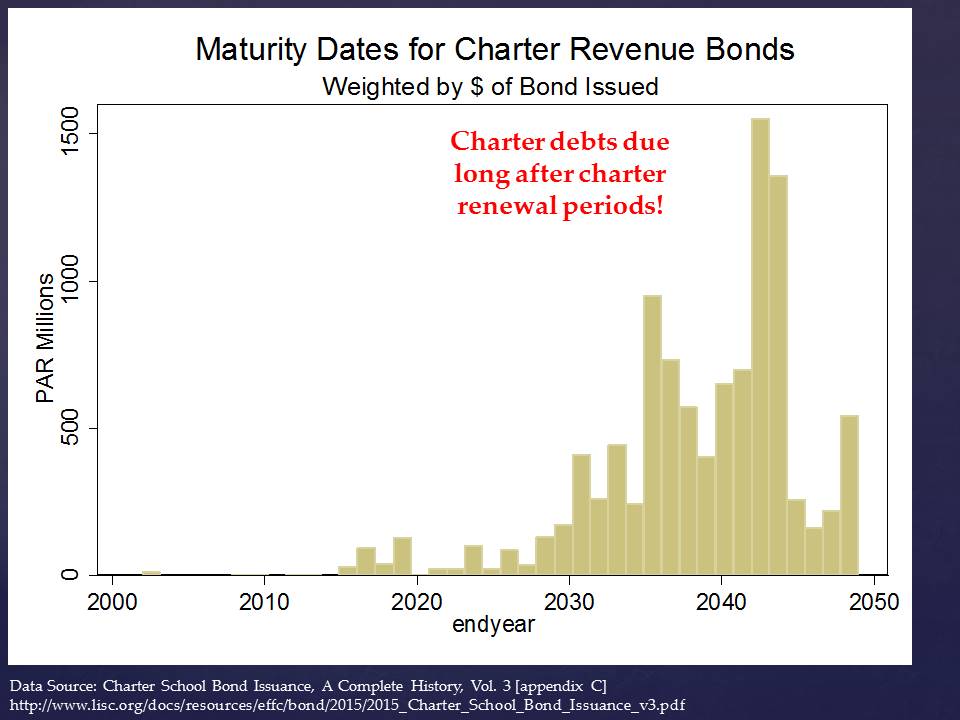

So how much of this debt is accumulating? And when does it come due? Who is issuing this debt? Are we looking at a charter school subprime bubble? Here are some snapshots:

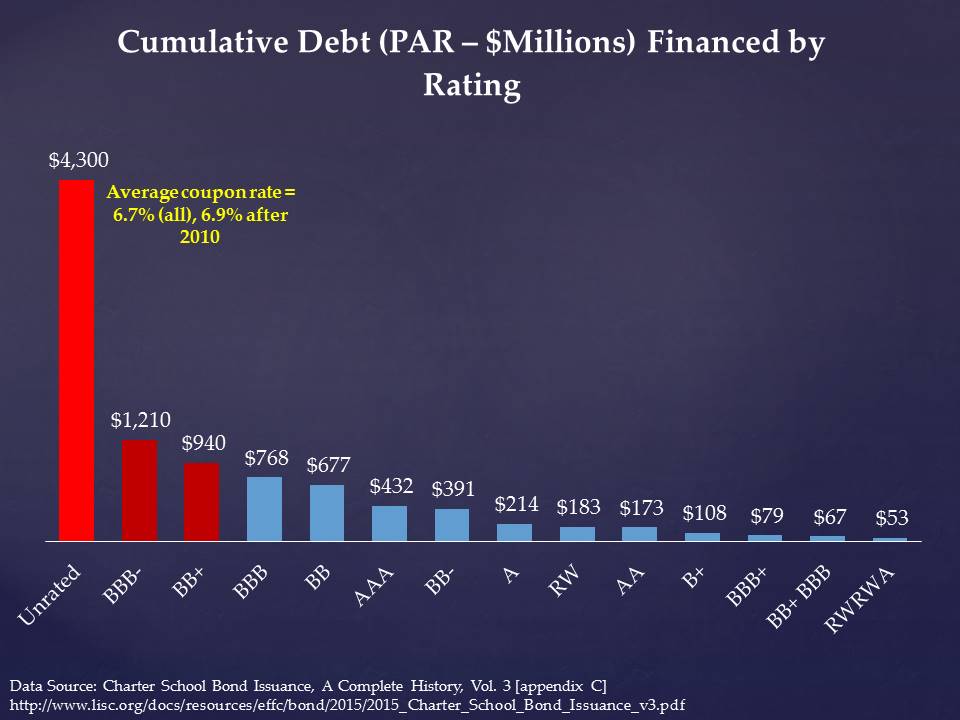

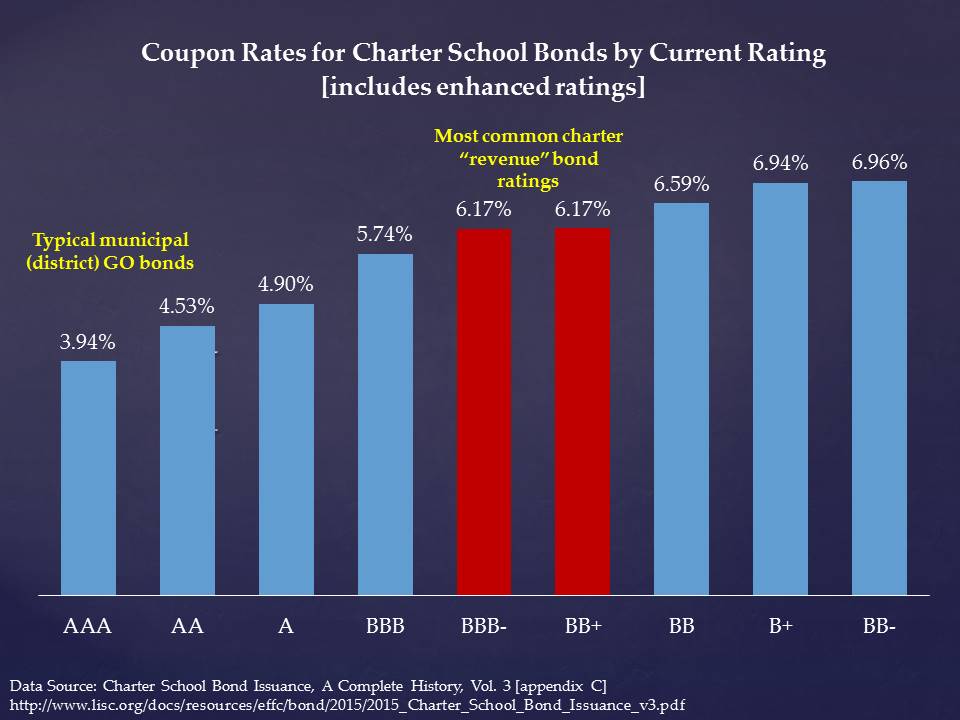

Most revenue bond debt incurred on behalf of charter schools is either unrated, or BBB- or BB+ rated. The unrated debt is saddled, on average, with coupon rates around 6.9% in recent years, marginally higher than rates attached to BBB- or BB+ bonds.

PIMA County Industrial Development Authority in Arizona has been particularly active in recent years! Still trying to figure this one out.

So, are we at risk of a subprime chartering collapse?

What will happen to all of this debt if some of the bigger charter chains go belly up? Can’t make their (at times exorbitant) lease payments?

Have we let the charter industry get “too big to fail?” [certainly by comparison, this is a tiny bubble, but it’s really just getting started]

And when and how will that bail out occur? [and who will own those facilities when the dust settles?]

Bruce Baker is an Professor in the Graduate School of Education at Rutgers, The State University of New Jersey. From 1997 to 2008 he was a professor at the University of Kansas in Lawrence, KS. He is lead author with Preston Green (Penn State University) and Craig Richards (Teachers College, Columbia University) of Financing Education Systems, a graduate level textbook on school finance policy published by Merrill/Prentice-Hall. Professor Baker has written a multitude of peer reviewed research articles on state school finance policy, teacher labor markets, school leadership labor markets and higher education finance and policy. His recent work has focused on measuring cost variations associated with schooling contexts and student population characteristics, including ways to better design state school finance policies and local district allocation formulas (including Weighted Student Funding) for better meeting the needs of students.

Baker, along with Preston Green of Penn State University are co-authors of the chapter on Conceptions of Equity in the recently released Handbook of Research Education Finance and Policy, and co-authors of the chapter on the Politics of Education Finance in the Handbook of Education Politics and Policy and co-authors of the chapter on School Finance in the Handbook of Education Policy of the American Educational Research Association.

Professor Baker has also consulted for state legislatures, boards of education and other organizations on education policy and school finance issues and has testified in state school finance litigation in Kansas, Missouri and Arizona. He is a member of the Think Tank Review Panel, a group of academic researchers who conduct technical reviews of publicly released think tank reports on education policy issues.

View all posts by schoolfinance101

Published

One thought on “Picture Post Week: Subprime Chartering”

One thought on “Picture Post Week: Subprime Chartering”

Comments are closed.